In this third part of our series on Private Equity Groups (PEGs), we will examine how PEGs perceive value. But first, we must define what it is that PEGs are valuing.

In almost all cases, when a PEG makes an offer for a company it is based on the Enterprise Value of the firm. The parts of the balance sheet the PEGs acquire are usually the tangible and intangible assets plus the net-working capital of the business where networking capital is defined as current assets minus current liabilities. Current assets are accounts receivable and material inventory, but often don’t include the cash on hand of the business while Current liabilities are accounts payable and other short-term obligations.

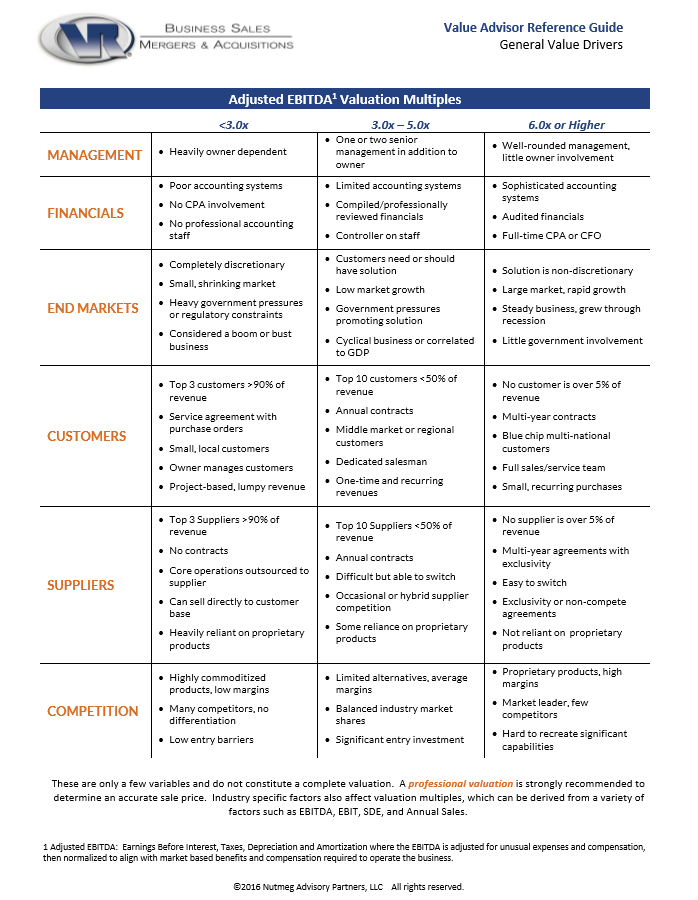

PEGs determine an enterprise value by applying a multiple to the adjusted EBITDA earnings of the business where adjusted EBITDA is defined as EBITDA that has been adjusted to normalize owner compensation and benefits. The multiple used typically runs in a range of between 3 and 6 times.

Whether a business sells for either 3 times or 6 times earnings or somewhere in-between is largely determined by how the company performs in six (6) areas;

- Management

- Financial Controls & Reporting

- End Markets

- Customers

- Suppliers

- Competition

By way of examples, a company with a strong management team is a more attractive investment than one that can’t operate without the owner. A company whose revenues are derived from clients who operate in good, growing markets has better value than one whose clients are in slow growing or flat industries. A company whose products or services rely on a few suppliers will trade for less than one that has a diversified vendor base. A company with limited customer concentration and very “sticky revenues” will sell for a higher price than one that relies greatly on one or two clients and does not have any contractual relationships with predictable revenue streams. When PEGs assign a multiple, they largely go through an exercise to assess the firm’s relative performance in each of these areas.

Even among these six categories, some categories are more important than others. Those that are more easily controlled by the owners such as Management and Financial Reporting are weighted less in a valuation than those areas that are more difficult to control such as End Markets, Customers, Suppliers and Competition. Companies that assess well in those areas that are more difficult to control achieve the highest valuations.

On the right is our Value Advisor Reference Guide. This document succinctly summarizes factors affecting the multiple range in each of the six areas. Every owner should review this to objectively assess what parts of their business are helping and which parts are hurting them in creating value. We can guarantee that buyers of any business are doing the same. Click here or on the picture to view.